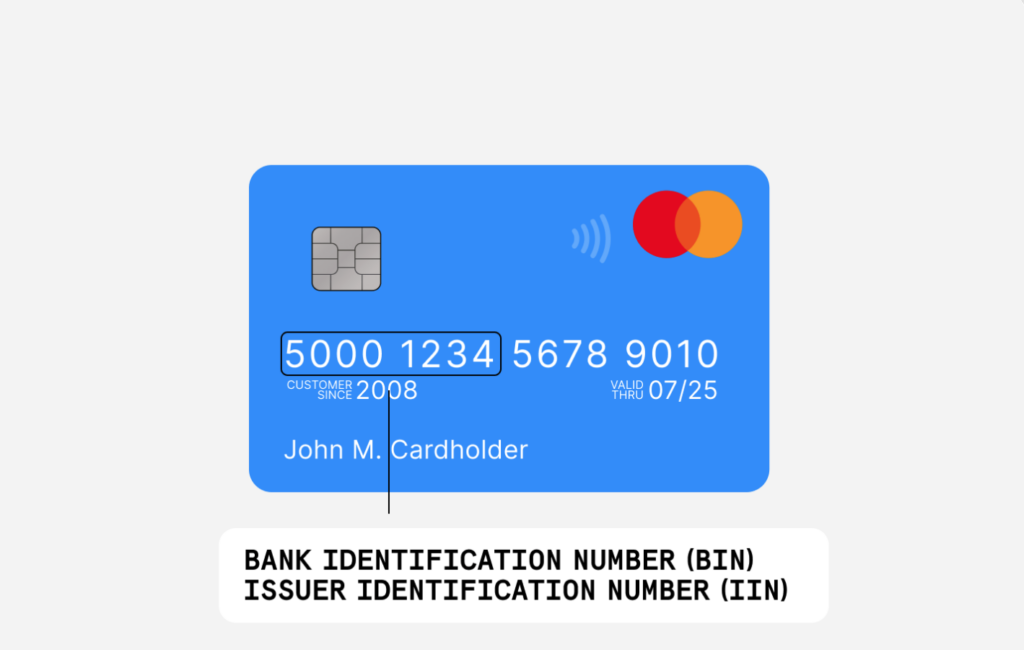

A Bank Identification Number (BIN) consists of the first four to six digits on any payment card. This number sequence exclusively identifies which financial institution issued the card, playing a vital role in routing transactions to the appropriate issuer. BINs appear across various card types—credit cards, debit cards, and charge cards alike—ensuring accurate transaction processing.

Understanding Bank Identification Numbers

The primary function of a BIN is enabling financial institutions to detect fraudulent transactions, including stolen cards, while helping to combat identity theft.

Bank Identification Number

How Bank Identification Numbers Function

BINs operate within a framework established by the American National Standards Institute (ANSI) and the International Organization for Standardization (ISO). These organizations developed protocols to identify card-issuing institutions. ANSI, a U.S.-based nonprofit, concentrates on establishing business standards domestically, whereas ISO sets industry benchmarks globally.

Also Read: Revised Bitcoin Carding Instructions 2026 –The Coin base Approach

Every payment card receives a distinct BIN comprising four to six digits. These numbers appear on the card’s front face and in the embossed text below. The initial digit designates the Major Industry Identifier (MII), while subsequent digits pinpoint the specific issuing bank or institution. For instance, Visa cards start with 4, categorizing them within the banking and financial sector.

When consumers make online purchases and input their card information, the system scans the first four to six digits. This allows merchants to identify the issuing institution and retrieve additional details such as:

- The card network (Visa, MasterCard, American Express, etc.)

- The card tier (platinum, corporate, standard, etc.)

- The card category

- The country where the issuing bank operates

Once a transaction begins, the issuing bank verifies the card’s legitimacy, available funds, and whether the purchase meets eligibility requirements. The system then either authorizes or rejects the charge. Without BINs, payment processors would face significant challenges confirming fund sources, effectively blocking transactions.

GET VERIFIED BINS HERE

Generating Complete Credit Card Numbers from BINs

Credit card numbers emerge through a sophisticated process beginning with the Bank Identification Number. The BIN occupies the first four to six positions of the card number, establishing the issuing bank and card type. Digital systems produce full credit card numbers by adhering to specific structural rules tied to the BIN.

The following digits (referred to as the account number) are randomly allocated by the issuing bank to create a unique identifier for the cardholder’s account. The final digit serves as the checksum, computed using the Luhn algorithm to validate the entire number. This methodology helps deter fraud and guarantees proper payment routing throughout transaction processing.

Grasping this mechanism allows merchants and consumers to conduct secure, efficient transactions.

The Role of Bank Identification Numbers

BINs serve essential functions in enabling seamless transactions and fraud prevention. They assist merchants in evaluating and authenticating card payments, creating smooth purchasing experiences. BINs also supply critical information including the issuing bank’s physical address and contact details, while confirming whether transactions originate from the same country as the cardholder.

A core BIN function involves protecting against identity theft. By comparing data such as the cardholder’s address against the issuing bank’s location, BINs can identify suspicious patterns that might indicate fraud or security breaches. Furthermore, BINs accelerate the payment process by enabling rapid validation during card swipes, promoting quicker and safer checkouts.

BINs in Action: A Practical Example

Consider a customer paying for gasoline at a service station. As the customer swipes their card, the payment terminal reads the BIN to recognize the issuing bank. This triggers an authorization request verifying the customer’s available funds. Assuming the account is legitimate and sufficient funds exist, the transaction receives approval; otherwise, it gets declined.

This Article Is Interesting: Up-To-Date Zelle Carding Method Step by Step: All What You Need To Know About Zelle Carding For Instant Cash Out

Bank Identification Code (BIC) Explained

A Bank Identification Code (BIC), sometimes called a bank identifier code, represents a specialized 8 to 11-character code employed for international transactions. The BIC becomes essential when executing cross-border payments. It may function as either a connected BIC within the SWIFT network or a non-connected BIC used primarily for reference purposes.

How Consumers Interact with BINs

Although consumers rarely engage directly with BINs, recognizing their importance offers advantages. The BIN’s first digit reveals the major industry category, while remaining digits indicate the issuing bank. With each transaction, the BIN assists in validating the account and determining fund availability.

Understanding BIN Fraud Schemes

BIN scamming represents a fraudulent tactic where criminals pose as bank representatives to manipulate victims. They might falsely claim that the cardholder’s information has been compromised in an effort to build trust. Once scammers gather sufficient details, they may attempt to verify the card number or extract additional sensitive data, including the complete BIN.

BINsBank Identification Number

Why BIN Numbers Matter

BINs occupy a central position in contemporary payment infrastructure. They not only support acceptance of multiple payment methods but also ensure transactions process efficiently and rapidly. By delivering crucial information about card issuers, BINs assist financial institutions in identifying stolen or compromised cards, thereby shielding both consumers and merchants from fraudulent activity.

Conclusion

To summarize, Bank Identification Numbers are fundamental to modern financial operations. They identify the financial institutions behind payment cards, enable secure transaction processing, and defend against identity theft. Consequently, safeguarding your BIN and other financial information remains crucial. Remember: legitimate banks never contact customers via phone or email to report security breaches. If you suspect fraudulent contact, terminate the communication immediately and reach out to your bank directly. Additionally, file a report with the FTC for additional support.